Internal Audit of COVID-19 Response Fund Management

Table of Contents

- 1. Conformance with Professional Standards

- 2. Background

- 3. Audit Objective, Scope and Methodology

- 4. Governance

- 5. Controls

- 5.1 Departmental Directives and Frameworks

- 5.2 Procedures

- 5.3 Financial Controls

- 5.4 Performance Indicators

- 6. Conclusion

- 7. Recommendations and Considerations

- 8. Management Action Plan

- Annex A: COV19 and HWF Deployment Process

- Annex B: Audit Criteria

- Annex C: Acts, Policies, Directives, Guidelines

- Annex D: Grant and Contribution Risk Mitigation Measures

1. Conformance with Professional Standards

This audit conforms to the Institute of Internal Auditors’ International Standards for the Professional Practice of Internal Auditing and the Government of Canada’s Policy on Internal Audit, as supported by the results of the Quality Assurance and Improvement Program.

2.0 Background

Emergency Management in Canada

The Emergency Management Act stipulates that the Minister of Public Safety and Emergency Preparedness is responsible for exercising leadership relating to emergency management in Canada. In this role, the Minister is responsible for coordinating, among government institutions, and in cooperation with the provinces and other entities, emergency management activities. Further, under the Emergency Management Act, the Minister is responsible for the coordination of Requests for Federal Assistance (RFAs). Within Public Safety Canada (PS), RFAs are managed by the Government Operations Centre (GOC).

COVID-19 Pandemic Response

The COVID-19 pandemic placed tremendous pressure on the health system of many jurisdictions and challenged the capacity of supporting organizations. The response to the COVID-19 pandemic and the stress that these efforts placed on provinces and territories resulted in the GOC receiving an unprecedented number of RFAs. From January 2020 to May 2023, PS received 150 RFAs from provinces, territories and federal organizations; pre-2020, the GOC only received a handful of RFAs each year.

As a result, the Government of Canada announced funding for non-governmental organizations (NGOs), which was provided through the following transfer payment programs:

- Supporting the Canadian Red Cross’ (CRC) Urgent Relief Efforts Related to COVID-19, Floods and Wildfires program (COV19)

- Supporting a Humanitarian Workforce to Respond to COVID-19 and Other Large-Scale Emergencies program (HWF)

The deployment of NGOs through the transfer payment programs became an additional option to respond to RFAs. An overview of the process used to deploy NGO(s) is outlined in Annex A. As the deployment of NGOs was tied to the RFA process, this created urgency and resulted in time pressures in order to respond to the emergency expeditiously.

PS COVID-19 Related Contribution Programs

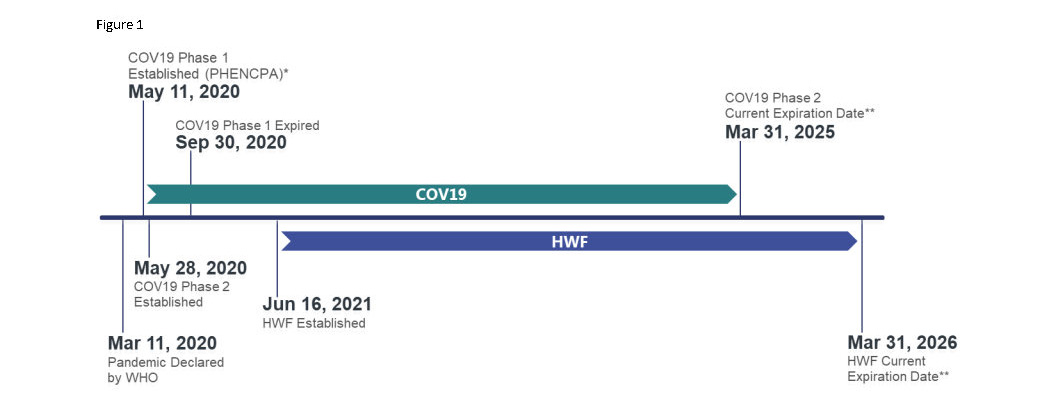

Given PS’s emergency management leadership role, funding was provided by the Government of Canada to administer the COV19 and HWF contribution programs. These programs were designed to respond and build capacity related to COVID-19 and other large-scale emergencies. The Figure below illustrates the timeline of the two programs.

Fig. 1. COV19 and HWF Programs Timeline

Image Description

Figure 1 is a timeline showing important dates of the COV19 and HWF programs. The important dates identified are:

- March 11, 2020: Pandemic Declared by the Word Health Organization (WHO)

- May 11, 2020: COV19 Phase 1 Established under the Public Health Events of National Concern Payments Act (PHENCPA)

- May 28, 2020: COV19 Phase 2 Established

- September 30, 2020: COV19 Phase 1 Expired

- June 16, 2021: HWF Established

- March 31, 2025: COV19 Phase 2 Current Expiration Date**

- March 31, 2026: HWF Current Expiration Date**

Each program is represented by an arrow that spans from its start to end date.

Note: the program expiration dates included are as of May 2023.

*Public Health Events of National Concern Payments Act (PHENCPA)

**Current Program Expiration Date as of May 2023

Supporting the CRC’s Urgent Relief Efforts Related to COVID-19, Floods and Wildfires program

The COV19 program utilized a directed solicitation process with the CRC as the sole recipient. An initial $100M in support to the Red Cross for urgent relief efforts related to COVID-19, floods and wildfires was announced by the Prime Minister in May 2020 and was provided in order to reduce the impact of these events on Canadians. The program provided for a wide variety of activities including, supporting public health and emergency response and recovery through risk reduction, virtual relief services, and deployment of emergency response units.

This funding was divided into two phases:

- Phase 1: Provided immediate funding of $40.68M to the CRC under the PHENCPA.

- Phase 2: Established Terms and Conditions for the Program, to provide up to $59.32M to the CRC.

In December 2020, up to $70M of additional funding was announced, which was comprised of:

- $35M secured for the program through a Treasury Board Submission; and

- $35M under the Safe Restart Agreement funding transferred to PS by Health Canada and administered under the PS contribution program.

Directed Solicitation Process

A solicitation process open to “one” applicant, based on an environmental scan and supported by a justification that only this organization holds the required expertise.

Supporting a Humanitarian Workforce to Respond to COVID-19 and Other Large-Scale Emergencies program

The HWF program provided funding to NGOs so that they may build capacity and deploy to respond to COVID-19 and other large-scale emergencies. The program supported two streams of activities: capacity-building and emergency response, which included the deployment of emergency response teams. The HWF program had an original funding amount of up to $150M, over two years. In spring 2023, authorities were secured to extend the program and its funding by three years, increasing the overall program funding level to $258.9M over five years.

The HWF program utilized a targeted solicitation process that pre-selected four NGOs for funding. Criteria for their selection was established in the Program’s Terms and Conditions, as well as a process for considering other organizations.

Targeted Solicitation Process

A solicitation process which is open to a specific type of applicant (e.g., academic institutions, provinces and territories, subject-matter experts).

Overview of Branches’ Roles and Responsibilities

The COV19 and HWF programs were designed and administered by the Emergency Management and Programs Branch (EMPB), with support from the Corporate Management Branch (CMB). A high-level overview of the roles and responsibilities of the relevant branches are identified below.

EMPB

Policy and Outreach Directorate

- Responsible for program design and related policy decision products (e.g., Memorandum to Cabinet and Treasury Board Submissions)

- Secretariat for the Deputy Minister Emergency Management Committee (DM EMC)

Programs Directorate

- Responsible for administration of COV19 and HWF which includes project administration from receipt of funding request to project close out

Government Operations Centre

- Leads RFA process

- Provides situational awareness and develops related products (e.g., Common Operating Picture)

- Secretariat for the ADM Crisis Cell

Regions

- Involved in RFA process for their respective region

CMB

Comptrollership

- Provides financial advisory services to branches and grant and contribution programs regarding financial budgeting, forecasting and reporting functions

Grants and Contributions Centre of Expertise (CoE)

- Provides support to branches to effectively manage PS’s grant and contribution programs by providing guidance to program directors, officers and administrators related to the delivery of grants and/or contributions

- Responsible for the development of PS’s Grant and Contribution related policy, directives, and other guidance documents

- Liaises with Treasury Board and reviews submissions

- Reviews Request for Project Approval Form (RPAF) that require Deputy Minister approval

- Responsible for the development and maintenance of the departmental Recipient Audit Plan as well as the related policy, directive, guidance, and tools that support the Plan

3. Audit Objective, Scope and Methodology

Objective

The objective of this audit was to assess governance, monitoring and reporting practices in place to manage and deliver on the PS COVID-19 related contribution programs (COV19 and HWF).

Scope Inclusions

The scope of the audit included transactions, records, and processes conducted by the EMPB and CMB under the COV19 and HWF programs. The period under examination was from March 2020 to June 2022.

Scope Exclusions

- The scope of the audit did not include:

- Funding agreements related to flood, wildfires and other large-scale emergencies,Footnote1 that did not include COVID-19; and

- The departmental recipient audit process, which is led by CMB.

Methodology

For each criteria established (Annex B), an audit methodology was developed to sufficiently and appropriately examine the area in support of the audit objective. To complete the audit, the following methods were used:

- Interviews: Interviews and walkthroughs were conducted with PS personnel in EMPB and CMB.

- Document Review: Relevant acts, policies and directives (Annex C); as well as program and project level documentation were reviewed.

- Data Analysis and Testing: Data from May 2020 to June 2022 was analyzed. selection of 20 agreements (10 COV19 and 10 HWF) were selected for examination. At the time of selection, the total population of agreements was 40 for both programs combined.

Future Engagement

A proposed evaluation of the HWF program is planned for 2025-26.

4. Governance

Finding: The governance structure was effective in supporting inter-departmental collaboration and provided direction through informed and timely decisions. However, the Terms of Reference (ToR) for the DM EMC was not current, and some expected elements were not included.

The governance structure established per the Terms and Conditions of the COV19 program included inter-departmental Assistant Deputy Minister (ADM) and Deputy Minister (DM) level committees. This structure was refined during the COV19 program as a result of the operational realities of responding to RFAs in an emergency context, which resulted in the removal of the ADM level committee from the project proposal endorsement process. These refinements were also reflected in the Terms and Conditions for the HWF program.

Assistant Deputy Minister Crisis Cell

During the COVID-19 pandemic, the Assistant Deputy Minister Crisis Cell (ADM Crisis Cell) was established with a mandate to monitor current and emerging issues in the management of COVID-19 and convene federal partners to coordinate a potential response. The ADM Crisis Cell’s membership included representatives from nine organizations, with the ability to add other representatives on an ad hoc basis.

The Terms and Conditions of the COV19 program included the ADM Crisis Cell as part of the application review and decision process for the program in advance of the DM EMC. One of the intended roles of the ADM Crisis Cell was to reach consensus to recommend a project proposal be brought forward to the DM EMC for consideration. However, the frequency of proposals and the need for timely reviews did not allow for the expedient administration of this function. This change was reflected in the HWF’s Terms and Conditions with the ADM Crisis Cell no longer included as part of the project proposal endorsement process.

Although the ADM Crisis Cell was not directly involved in the project proposal endorsement process, they provided broader situational awareness of the overall COVID-19 landscape. This demonstrated the necessary governance flexibility given the unprecedented circumstances and put them in a position to assist in refining and understanding the needs of provinces and territories, as well as anticipating future resource requirements.

ADM Crisis Cell Standing Member Organizations

- Public Safety Canada

- Health Canada

- Public Health Agency of Canada

- Privy Council Office

- Canadian Armed Forces

- Indigenous Services Canada

- Crown-Indigenous Relations and Northern Affairs Canada

- Canadian Border Services Agency

- Transport Canada

Deputy Minister Emergency Management Committee

In response to the COVID-19 pandemic, the DM EMC was struck to oversee and coordinate emergency management in conjunction with the provinces and territories. The secretariat responsibilities for the Committee resided in EMPB’s Policy and Outreach Directorate.

A ToR for the DM EMC was established at the onset of the pandemic, in March 2020, and included the following mandate:

- Monitor COVID-19 trends to assess risk, prepare for and respond to events requiring federal government, provincial and territorial emergency management responses.

- Triage and prioritize the deployment of federal resources and assets, particularly as it relates to formal RFAs from provinces and territories.

- Exercise urgent operational leadership and provide strategic advice to Ministers on horizontal emergency management responses.

DM EMC membership was comprised of 10 federal organizations’ deputy heads with operational responsibilities and authorities, complemented by central agencies. Further, the ToR established that “Deputy Heads from other relevant departments and agencies are invited to participate depending on the issue.”

Part of the DM EMC’s roles and responsibilities was to perform a review and endorsement function for COV19 and HWF proposals. These reviews were informed by regular situational reports on the COVID-19 landscape, such as the Common Operating Picture produced by the Government Operations Centre. To assist future deployment decisions, EMPB Programs Directorate developed a Program Tracker designed to inform the Committee on commitments and forecasts.

The use of the DM EMC as an endorsement body enabled timely collaboration, at the highest level, between federal organizations involved in the pandemic response. Final funding decisions were made by the appropriate delegated authority at PS through the approval of the Request for Project Approval Form (RPAF).

Terms of Reference was not maintained

Since the establishment of the ToR by the DM EMC in March 2020, there was no documentation to support a revised version being adopted by the Committee even though changes took place that should have resulted in updates.

- For example, a co-chair for the committee was introduced on May 16, 2022, however, this change was not reflected in the ToR.

Although updates to the ToR were drafted in September 2021, which provided greater detail on: quorum; official alternates; and, an expansion of the roles and responsibilities within the mandate, they were not formally adopted by the Committee.

In discussions with Policy and Outreach Directorate in January 2023, it was confirmed that the March 2020 version was still in effect.

Not maintaining and ensuring the ToR accurately captured the current state of the Committee, resulted in an outdated description of the roles, responsibilities and operations of the Committee.

DM EMC Standing Members

- Public Safety Canada

- Health Canada

- Public Health Agency of Canada

- Transport Canada

- Natural Resources Canada

- Agriculture and Agri-Food Canada

- Department of National Defence & Canadian Armed Forces

- Justice Canada

- Privy Council Office:

- Intergovernmental Affairs

- Operations

- National Security and Intelligence Advisor (NSIA)

- Treasury Board

Recommendation: Going forward, the ADM, EMPB should ensure any ToR for the DM EMC is updated, approved and communicated to reflect the Committee’s current state.

Greater clarity on quorum and consistent documentation of decisions were required

One of the DM EMC’s main functions was to review and endorse project proposals. The endorsement process took place either through scheduled meetings or secretarially in order to provide timely decisions given the urgent nature of the requests. As part of this process, the audit team expected decisions to be documented and quorum requirements addressed at the onset of the programs.

Although the project proposal endorsement process consistently incorporated opportunities for collaboration with members, there were instances where the input of organizations was either not provided or not included in the project documentation. For example, when endorsements were sought during committee meetings, the “summary of meeting” document did not consistently identify the organizations in attendance. This created gaps in the documentation of decisions.

There were also documentation issues related to projects that were circulated secretarially. In one example, a federal organization was not consulted on the original DM EMC request for endorsement but was subsequently consulted when a request for endorsement was brought to DM EMC for an amendment to the project. In such cases, the audit team did not identify documentation to demonstrate why a non-standing member organization was included as part of the project proposal endorsement process.

In March 2020, the ToR adopted by the DM EMC did not identify the quorum required to endorse a project proposal. Further, interviews demonstrated differing interpretations of quorum requirements between policy and program staff at PS.

- The Policy and Outreach Directorate, responsible for the DM EMC Secretariat, did not identify a set figure.

- Program staff informed the audit team that they considered a proposal endorsed if critical mass was received, along with responses from the Privy Council Office and Treasury Board Secretariat.

- Program staff commented that this approach to quorum had been communicated to the ADM of EMPB, however this decision was not reflected in any governance artifacts.

The lack of defined quorum requirements increased the risk of a project being considered endorsed without receiving the required support. This issue was compounded by the consistent use of pre-execution of expenditures, which allowed for the recipient to start incurring costs following DM EMC endorsement but preceding delegated approval via the RPAF.

While there may have been varying interpretations of what constituted quorum, the audit team did not identify any instances where a DM EMC member organization proposed not to fund a project or opposed the funding of a project.

Consideration: When establishing a governance committee, consideration should be made to ensure quorum requirements are established and documented in the ToR to ensure clarity surrounding the endorsement and approval process. This is of particular importance where pre-execution expenditures are allowable.

5. Controls

5.1 Departmental Directives and Frameworks

Finding: There were inconsistencies in the interpretation and application of departmental directives and frameworks.

Established directives and frameworks are intended to provide for a consistent application of processes, procedures, and decision making. In assessing the COV19 and HWF project files, the audit team examined the use and application of relevant departmental directives and frameworks.

Pre-Execution Expenditures Directive

Pre-execution expenditures are costs incurred by a recipient, under exceptional circumstances, prior to the signing of an agreement. This allows a recipient to begin incurring eligible costs without having to wait for an agreement to be in place. Under COV19 and HWF, pre-execution of expenditures was utilized in nearly all files examined due to the urgent need for recipients to respond and/or deploy.

The departmental Directive outlines various requirements prior to the issuance of pre-execution expenditures, including:

- Explicit authorization in the programs’ terms and conditions;

- A signed exception form, approved at the Director General level, authorizing pre-execution expenditures before the contribution agreement was signed.

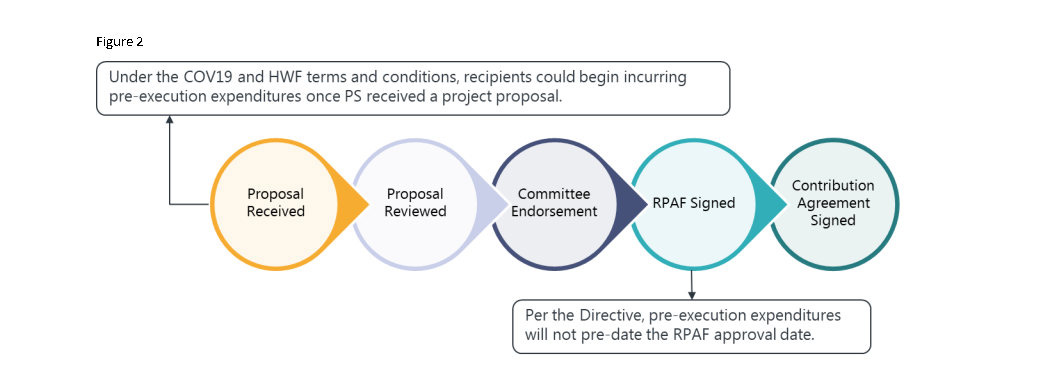

The terms and conditions of both programs allowed for eligible expenditures to be incurred earlier in the process, at receipt of the project proposal, than what is described in the Pre-Execution Expenditures Directive (see Figure 2).

The modification of when pre-execution expenditures could be incurred resulted in the recipient not having to wait for the expenditure initiation (i.e., RPAF) and/or the contribution agreement to be signed. This change supported timely NGO deployment in response to RFAs and, under capacity building projects, ensured NGOs had the ability to acquire the appropriate resources to support their response to potential future RFAs.

However, it should be noted that DM EMC and expenditure initiation approval remained necessary for PS to authorize the reimbursement of eligible expenditures.

Fig. 2. Commencement of Pre-Execution Expenditures

Image Description

Figure 2 shows the high-level process from when a proposal is received to when the contribution agreement is signed. The process consists of the following:

- Proposal received

- Proposal reviewed

- Committee endorsement

- Request for Project Approval Form (RPAF) signed

- Contribution agreement signed

Arrows have been included to indicate the point when pre-execution could start under the COV19 and HWF terms and conditions compared to the Department’s Pre-Execution Expenditures Directive.

Under the COV19 and HWF terms and conditions, recipients could begin incurring pre-execution expenditures once PS received a project proposal as early as step 1.

Per the Directive, pre-execution expenditures will not pre-date the RPAF approval date, which takes place in step 4.

According to the Pre-Execution Expenditures Directive, the use of an exception form was mandatory for the authorization of pre-execution expenditures. The exception form requires program officers to provide a justification for the specific requirement(s) of the directive(s) for which an exception is sought.

In discussing the use of exception forms with EMPB Program staff, their understanding was that regardless of what requirement(s) was/were identified it applied to the entire directive once the exception was approved. While the CoE, responsible for policy related guidance, explained that when an exception to a directive is sought, the exception form should indicate all requirement(s) the program is seeking an exception from.

Further, most of the exceptions being sought related to conditions which were already permissible under the terms and conditions of the programs, whereas aspects of the Directive’s reporting requirements, not identified in the exception form, were not met. As such, the use and purpose of the exception form in relation to the two programs was unclear.

Without clear guidance in place on the appropriate use of the exception form, it is difficult to ensure compliance with the Pre-Execution Expenditures Directive.

Exceptional Circumstances

There would have been loss of a critical project resource, or the viability of the project would have been jeopardized if the expenditures had not been incurred prior to the signature of the agreement.

Recommendation: The ADM, CMB should ensure that programs are provided with clear guidance on the requirements and use of exception forms to help ensure consistent application.

Advance Payments

Along with the use of pre-execution expenditures, the Terms and Conditions of the COV19 and HWF programs allowed for the use of advance payments under exceptional circumstances, if they were requested by the recipient organization and supported by appropriate documentation (i.e., cashflow statements and/or financial statements).

In the 10 files examined, that contained advanced payments documentation in support of the recipient’s request for advance payments was not on file. This made it challenging to assess whether an advance payment met the threshold described in the terms and conditions of the programs. In discussions with EMPB Programs Directorate, ongoing cashflow issues were communicated by recipients however no documentation was on file to support the use of advance payments.

In June 2021, the PS Project Risk Management Directive was updated and approved. It provides additional guidance in instances where recipients are eligible for advance payments.

In order for advance payments to be included in the contribution agreement, the recipient must demonstrate that advance payments are essential to achieving the objectives of the project. This can be demonstrated through one or more of the following:

- Financial statements from previous years

- Bank statements and letters

- The need to cover basic expenditures such as salaries and rent for the project/initiative in question

The 2021 Directive also requires the Recipient Advance Justification Form to be submitted by the recipient and approved by PS. This requirement came into effect May 1, 2022.

Several of the projects examined included an Exception Form for the use of advance payments. Although, the CoE indicated that the exception form was not applicable to this type of payment, advance payments were listed as a category on the form. More clarity on the use of the exception form could assist in reducing administrative burden while ensuring appropriate approval for advance payments.

Advance Payments

Payments, specifically provided for in the funding agreement for a contribution, that are made before the performance obligations of the funding agreement that would justify payment of the contribution have been met.

Recommendation: The ADM, CMB should ensure that programs are provided with clear guidance on the requirements and use of exception forms to help ensure consistent application.

Project Level Risk Management

The PS Project Level Risk Management Directive provides formal direction to ensure uniformity in process and decision making across the department in the areas of risk identification, assessment and mitigation strategies for Grants and Contributions projects at PS. The completion of a risk assessment is required at the onset of a project; annually during a project; and when an amendment is required, unless an exception to the Directive is sought.

At the time of the engagement, the Directive included six factors (Table 1), which were identified as potential risks to the effective delivery and achievement of results. The Program Officer determined the project’s risk level for all files examined, using the risk assessment tool, by assessing the project against the six factors. Once the project was assessed, the corresponding mitigation strategies, as outlined in Annex D, were applied.

| Risk Factor | Definition |

|---|---|

| Agreement Materiality | Total PS funding provided. |

| Recipient Capacity | The recipient’s capacity to successfully deliver, manage and report on the agreement and the funding, and achieve its stated objectives, including capacity to meet the requirements of the official languages act, as required. |

| Previous Grant and Contribution Experience | Experience with Public Safety and/or other levels of government on previous grant and contribution agreements/projects. |

| Agreement Feasibility | The activities outlined in the agreement and the difficulty associated with achieving the desired objectives. |

| Third Party Involvement | Arrangements that exist for the agreement in terms of the type of partner, the number of partners, the experience of the recipient with these partners, and the confirmation of funds from partners. |

| Agreement Sensitivity | The degree to which the agreement may be scrutinized by the public. |

The audit team noted that EMPB Programs consistently carried out risk assessments and applied mitigation strategies in accordance with the Directive. The majority of the 20 projects sampled were assessed as low risk (Table 2).

As the assessment tool only includes the six factors, project specific risks (e.g., the use of pre-execution expenditures and advance payments) that may increase the overall risk to the Department are not accounted for in the risk assessment. For example, in one instance the Program sought an exception to the Directive in order to increase the frequency of reporting related to a low-risk project. The justification of exception referenced the amount of funding being provided; the use of advance payments; and recent reporting experience with the recipient. Given this project occurred later in the sample it is unclear whether this practice continued.

Although EMPB Programs Directorate complied with the requirements of the Directive, the risk assessment tool did not allow for flexibility in accounting for factors that may have impacted the results and selection of mitigation strategies.

| Risk Level* | COV19 | HWF |

|---|---|---|

| Low | 9 | 9 |

| Medium | 1 | 1 |

| High | 0 | 0 |

*As certain projects included multiple risk assessments, the table reflects the highest level of risk associated with the project.

5.2 Procedures

Finding: Documentation in support of the project proposal requirements, as established in the programs’ terms and conditions, was not consistently on file.

As part of the administration of the COV19 and HWF programs, tools and procedures were established to help ensure agreements complied with the terms and conditions of the programs.

Project Proposal Templates

The terms and conditions of both programs established requirements that the recipient must address when submitting a proposal to PS.

Under the COV19 Program, modifications were made to the original proposal template in order to reduce the administrative burden by removing duplications using a streamlined proposal form. This was done by omitting organizational level information given the program had one recipient. Project risks and Gender-based Analysis Plus (GBA Plus) information were also removed from the streamlined form as they were deemed similar across projects. Despite this, project risks and GBA Plus were still required to be addressed for each project per the Terms and Conditions. This created a gap between the proposal requirements in the Terms and Conditions and the information required in the streamlined proposal form.

Program staff communicated that some of the elements removed from the proposal may have been addressed through conversations with the recipient, however these conversations were not consistently documented. Given the COV19 Terms and Conditions required proposals to cover the removed elements, the audit team expected to find supporting documentation demonstrating how they were addressed.

Under HWF, an updated version of the proposal form was used. This version contained additional supporting details that were removed from the streamlined form. This included but was not limited to:

- More detailed information on populations benefiting from the project;

- A description of the involvement of partners or other organizations that may be participating; and,

- An explanation of the project’s objective(s) and expected outcome(s).

Under the Capacity Building Stream, the HWF Program used a proposal form similar to the original proposal form utilized under the COV19 Program. Given the time and dollar commitment associated with capacity building projects, more detailed information was required in the proposal form. These elements included:

- Identification of potential project implementation risks that may impact the recipient’s ability to deliver on the project, and mitigation measures to address them; and,

- A description of the internal measures to conduct implementation monitoring and performance management.

The HWF Terms and Conditions allowed for more flexibility in addressing proposal requirements compared to COV19, as certain elements could be addressed outside the project proposal if they were done prior to the execution of the funding agreement. However, it was not always evident in the documentation whether these elements were addressed. In discussion with EMPB Programs Directorate, it was communicated that some of the elements may have been addressed through conversations, but documentation was not on file.

Consideration: When modifying a project proposal form, the ADM, EMPB should consider whether the requirements of the terms and conditions are/will be met.

Project Proposal Review

The proposal review process and supporting tools were modified over the course of the COV19 and HWF programs.

Under the terms and conditions of the programs, the PS Program Officer was responsible for the initial review and analysis of the proposal in advance of the DM EMC review. The review was intended to act as a challenge function to ensure a complete and appropriate proposal.

Following the initial review by the program officer, a collective review was conducted by representatives from the Policy and Outreach Directorate; Government Operations Centre; and relevant regional office. The purpose of this collective review was to validate whether the proposal would meet the required needs of the request by leveraging the perspectives of other sections within EMPB. While this process was not well documented under COV19, the HWF Program implemented a more formalized approach in early 2022 through the establishment of the Humanitarian Workforce Program Application Review Team, which was guided by a ToR.

To help facilitate the proposal review process, various tools were utilized by program officers. Under COV19, a Proposal Evaluation Guide was used, however, its use was minimal as it was found to impede timely and effective decision making. An Eligibility Checklist was later introduced to assist program officers in assessing proposals against the terms and conditions. The use of the Checklist was introduced under COV19 but was more consistently documented under the HWF program. This aided program officers in applying a more consistent approach to the proposal review process.

As part of the review, program officers were required to assess the budget in order to determine if expenditures were eligible under the terms and conditions. The audit team noted that the budget was provided at the cost category level and did not consistently include a detailed breakdown of expenditures, which created challenges in assessing the eligibility of expenses.

For example, one of the eligible expenditure categories was “Program supplies and materials ($10,000 or less per acquisition)”. However, upon review of a file which utilized this cost category, where the total expenditure was $160,500, the audit team could not find a breakdown of the expenditure in order to confirm that the limit of $10,000 per acquisition was followed.

In some instances, further clarification of cost categories was sought by program officers through ongoing communication with the recipient; however, documentation of these exchanges were not consistently on file.

Additionally, it was observed that an expenditure category not included under the Terms and Conditions was used. As per the Terms and Conditions, other costs can be covered by the Program “as approved in writing by the Minister of Public Safety and Emergency Preparedness,” however no such approval was on file.

Similarly, other files examined contained the use of the “other costs” category, however no documentation was on file demonstrating the required written ministerial approval.

Overall, review processes adapted to the urgency and volume of requests over the course of the programs. Although eligible cost categories were used in most cases, it is difficult to determine whether expenditures under cost categories within the budget were eligible without a detailed breakdown.

Recommendation: The ADM, CMB, should ensure the audits included in the Departmental Recipient Audit Plan related to COV19 and HWF are completed as scheduled. Based on the results of these recipient audits, consideration should be given to expanding the number of agreements included in the Audit Plan given the limited documentation on file to support financial information.

5.3 Financial Controls

Recommendation: The ADM, CMB, should ensure the audits included in the Departmental Recipient Audit Plan related to COV19 and HWF are completed as scheduled. Based on the results of these recipient audits, consideration should be given to expanding the number of agreements included in the Audit Plan given the limited documentation on file to support financial information.

Finding: Overall, the required section 32 and section 34 authorizations were obtained, however, there was limited documentation on file in support of expenditures which created difficulties in determining their appropriateness.

Financial controls enable an organization to effectively monitor and direct financial resources. As part of the COV19 and HWF programs, the audit team assessed the use and application of relevant financial controls.

Delegation of Authority

The Delegation of Financial Signing Authorities (DFSA) Instrument provides the level of financial signing authorities required to exercise responsibilities.

In the files examined, commitment authority (Section 32) and certification authority (Section 34) approvals were provided at the correct level as indicated in the DFSA instrument and were signed by the correct individual as per their Financial Authority Specimen Signature Record (FASSR). In addition, the RPAFs and Amended RPAFs examined were also signed at the appropriate level per the DFSA instrument.

Reasonability of Proposed Budget

In addition to the determination of the eligibility of expenditures, program officers also assessed the reasonableness of the proposed budget. As previously mentioned, the limited breakdown of expenditure categories impeded the program officer’s ability to assess the reasonableness of the budget.

Basis of Payment

In accordance with the Contribution Agreement’s Reporting Requirements and Payment Schedule annex, recipients were required to submit cashflow statements and non-financial activity reports as a basis of payment. As part of this submission, recipients were required to make the following attestation:

"I hereby certify that the attached itemized Statement of Revenues and Expenditures presents fairly the revenues received and the expenditures incurred by the Recipient for the period specified. Public Safety and Emergency Preparedness Canada may at any time request supporting documents for audit purposes."

Upon submission of required reports, program officers conducted a review of the cashflow statement and/or non-financial activity report. In the projects examined, supporting documentation, such as invoices, were generally not on file. Through discussions with EMPB personnel, a request for substantiation in support of actual expenditures typically depended on the risk level of the agreement. Given most agreements examined were assessed as low risk, minimal requests for substantiation were made.

Through file review and interviews, forecasting was identified as an ongoing issue, which resulted in over reported expenditures.

There were several instances where the use of advance payments resulted in overpayments. These were often resolved through deductions on upcoming payments to the recipient, either as part of the same project or as part of a different project. For these overpayments, an Accounts Receivable was created and the recipient was sometimes notified through a signed “Notice of Overpayment.” Payment issues of this nature increased the administrative burden to EMPB.

In a separate project examined, there were over-reported expenditures in the amount of $3.4M which went undetected by PS but were later disclosed by the recipient. The original project required an extension, however, due to time limitations around the program’s extension in relation to year-end activities, an amendment was not possible. Consequently, a new agreement (i.e., project) was created. The separation of the activities under these projects increased the complexity of reporting for the recipient and made it more challenging for PS to validate reports.

In this case, the review process of the cashflow statements and non-financial activity reports did not identify this discrepancy. Other than through the Departmental Recipient AuditFootnote2 process, which was not examined as part of this audit, it is difficult to determine whether this amount would have eventually been identified if the recipient had not disclosed the issue.

Recommendation: The ADM, CMB, should ensure the audits included in the Departmental Recipient Audit Plan related to COV19 and HWF are completed. Based on the results of these recipient audits, consideration should be given to expanding the number of agreements included in the Audit Plan given the limited documentation on file to support financial information.

5.4 Performance Indicators

Finding: Performance indicators were identified and established at the onset of the program, however there were challenges associated with reporting.

In order to assess performance, the COV19 and HWF programs were required to report on corporate performance indicators (i.e., service standards), as well as program level performance indicators established in the Terms and Conditions and at the project level through non-financial reporting requirements.

Service Standards

Service standards are a public commitment to a measurable level of performance that clients can expect under normal circumstances to potential recipients. PS established three service standards for all transfer payment programs to adhere to, which are publicly reported on. These service standards relate to the acknowledgement of the request, communication of a funding decision, and the issuing of payment.

Of the files reviewed, there were several instances where the documentation in the information management system did not support the date entered for the service standard.

Further, there was a discrepancy between departmental guidance documents and the interpretation by EMPB and CMB personnel regarding the requirement to track service standards for amendments.

The PS Funding Agreement Amendment Directive included, as part of the roles and responsibilities of managers and program officers, the inputting of data in support of departmental service standards requirements. Similarly, the PS Guidelines on Performance Service Standards for Transfer Payment Programs in place at the time of the projects, outlined that service standard one should be tracked for amendments requested by the recipient.Footnote3

However, EMPB Programs Directorate and CoE personnel shared the same understanding that service standards related to the acknowledgement of the request and communication of a funding decision were not reported on for amendments. This understanding differed from the applicable guidance in place at the time of the projects.

Recommendation: The ADM, CMB should ensure guidance surrounding service standard information clearly and consistently states whether amendment information is to be included or not as part of the reporting on service standards.

Program and Project Performance Reporting

In terms of program level performance, numerous indicators were included in the Terms and Conditions of the program under the expected results section, which were generally aligned with the results appendix in each of the funding requests. The data in support of these indicators were collected through recipient reports and were included in Public Safety’s Departmental Results Report.

In analyzing the indicators, the audit team acknowledged that establishing targets for the indicators at the onset of the program may have been challenging given the evolving and unpredictable nature of the pandemic situation. Further, some of the indicators included may have been difficult to report upon and in one instanceFootnote4 the Program was not able to provide results for the Departmental Results Report “as not all reports included this information.”

At the project level, the non-financial activity report outlined the activities undertaken in support of the approved project and was included in all files examined. The template for the report was annexed to the Contribution Agreement which identified the information the recipient was required to collect and report upon. A completed report was required for payment in accordance with the Contribution Agreement’s Reporting Requirements and Payment Schedule. However, late reporting was a common occurrence in the files examined.

For the majority of files tested, information on diversity and inclusion and/or GBA Plus was not consistently collected and reported on. Although there may have been challenges in collecting this type of information (e.g., privacy, capacity constraints), given this report was a requirement for payment, it was expected that the form would be fully completed, and rationales be provided in instances where information was not collected. Although the missing information created issues with regards to corporate reporting, EMPB Programs Directorate communicated that overall, they had enough information to respond to reporting requirements.

There were also instances where the recipient personalized the activity reports and in some cases the information provided did not align with the template annexed to the Contribution Agreement. This issue was identified by program officers and noted frequently in the comments section of risk assessments. It was communicated, that additional steps had been taken by EMPB Programs Directorate to address reporting issues, including bi-weekly meetings with the recipient; an increase to the risk level; and an extension to reporting timelines. However, these mitigating steps did not result in improvements.

Overall, there were challenges related to reporting which were impacted by the volume and speed at which projects were being administered. However, given these reports were requirements for payment, and the data collected could inform future responses to large scale emergencies (e.g., GBA Plus) the audit team expected further implementation of escalation protocols to ensure reports were as complete and timely as possible.

6. Conclusion

In response to the COVID-19 pandemic, PS was responsible for administering the COV19 and HWF contribution programs. In examining these programs, the audit concluded the following:

Governance

Overall, the governance structure met the needs of the programs by facilitating the management and delivery of the PS COVID-19 related contribution programs. However, the ToR for the DM EMC was not maintained and did not establish quorum requirements.

Monitoring and Reporting Controls

Additional guidance is required to help ensure monitoring and reporting controls are applied more consistently. Further, in assessing reports, the audit team was limited in their ability to validate compliance with funding agreement requirements given inconsistencies in supporting documentation.

7. Recommendations and Considerations

As a result of this engagement, the following recommendations and considerations have been identified. While recommendations are subject to the Internal Audit and Evaluation Directorate's management action plan follow-up process, considerations are not included given they are for management's consideration.

Recommendations

- Going forward, the ADM, EMPB should ensure any ToR for the DM EMC is updated, approved and communicated to reflect the Committee’s current state.

- The ADM, CMB should ensure that programs are provided with clear guidance on the requirements and use of exception forms to help ensure consistent application.

- The ADM, CMB, should ensure the audits included in the Departmental Recipient Audit Plan related to COV19 and HWF are completed as scheduled. Based on the results of these recipient audits, consideration should be given to expanding the number of agreements included in the Audit Plan given the limited documentation on file to support financial information.

- The ADM, CMB should ensure guidance surrounding service standard information clearly states whether amendment information is included or not as part of the reporting on Service Standards for Transfer Payment Programs.

Considerations

- When establishing a governance committee, consideration should be made to ensure quorum requirements are established and documented in the ToR to ensure clarity surrounding the endorsement and approval process. This is of particular importance where pre-execution expenditures are allowable.

- When modifying a project proposal form, the ADM, EMPB should consider whether the requirements of the terms and conditions are/will be met.

8. Management Action Plan

Recommendation 1

Going forward, the ADM, EMPB should ensure any ToR for the DM EMC is updated, approved and communicated to reflect the Committee’s current state.

Actions Planned

The ToR for the DM EMC will be revised and updated as per the recommendation in the report (Audit Report Ref.1). Once finalized and approved, the updated ToR will be communicated to reflect the Committee’s current state.

Target Completion Date

August 2023

Recommendation 2

The ADM, CMB should ensure that programs are provided with clear guidance on the requirements and use of exception forms to help ensure consistent application.

Actions Planned

- Ensure that programs are provided with clear guidance on the requirements and use of exception forms.

- Review the Directive on Pre-Execution Expenditures Directive to ensure clarity that allows for consistent application.

Target Completions Date

- March 2023

- August 2024

Recommendation 3

The ADM, CMB, should ensure the audits included in the Departmental Recipient Audit Plan related to COV19 and HWF are completed as scheduled. Based on the results of these recipient audits, consideration should be given to expanding the number of agreements included in the Audit Plan given the limited documentation on file to support financial information.

Actions Planned

- Continue to coordinate the list of projects for the 3-Year Recipient Audit Plan (3YRAP) and ensure that COV19 and/or HWF audits included in the 2023-24 to 2025-26 3YRAP are completed as scheduled.

- Based on the recipient audit results of the related projects audited in a), if these audits identify major findings, the number of audits conducted for COV19 and/or HWF programs may be expanded accordingly. If audit findings are not consequential, no additional audits will be conducted.

Target Completions Date

- June 2025

- To be assessed after scheduled audits are completed

Recommendation 4

The ADM, CMB should ensure guidance surrounding service standard information clearly states whether amendment information is included or not as part of the reporting on Service Standards for Transfer Payment Programs.

Actions Planned

- Communicate with stakeholders guidance that clearly states whether amendment information is included as part of the reporting on Service Standards for Transfer Payment Programs.

- Update existing training and reference materials to ensure clear guidance on service standards reporting.

Target Completions Date

- May 2023

- May 2023

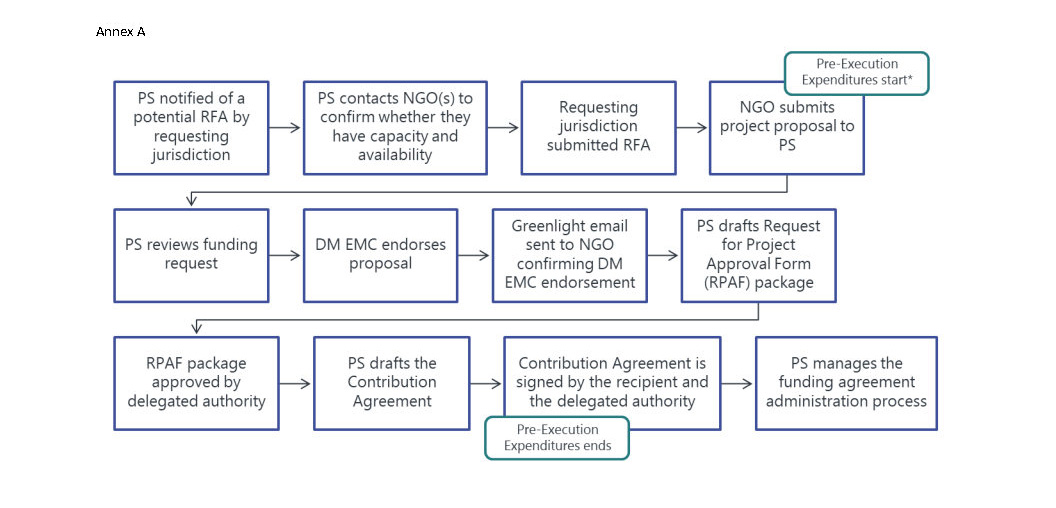

Annex A - COV19 and HWF Deployment Process

The following outlines the deployment process used in instances when an RFA triggered the deployment of NGO(s).

Image Description

Annex A is a diagram that outlines the deployment process used in instances when an Request for Federal Assistance (RFA) triggered the deployment of non-governmental organizations (NGOs). The steps are as follows:

- PS notified of a potential RFA by requesting jurisdiction;

- PS contacts NGO(s) to confirm whether they have capacity and availability;

- Requesting jurisdiction submitted RFA;

- NGO submits project proposal to PS.

- PS reviews funding request;

- The Deputy Minister Emergency Management Committee (DM EMC) endorses proposal;

- Greenlight email sent to NGO confirming DM EMC endorsement;

- PS drafts Request for Project Approval Form (RPAF) package;

- RPAF package approved by delegated authority;

- PS drafts the Contribution Agreement;

- Contribution Agreement is signed by the recipient and the delegated authority;

- PS manages the funding agreement administration process.

Under the terms and conditions of both programs, NGOs were allowed to start incurring pre-execution expenditures after receipt of a project proposal (i.e., step 4). Eligible expenditures would only be covered in special circumstances, if the project was approved. The use of pre-execution expenditures allowed NGOs to rapidly deploy in responding to RFAs. The use of pre-execution expenditures ends in step 11.

*Under the Terms and Conditions of both programs. NGOs were allowed to incur pre-execution expenditures after receipt of a project proposal by PS. Eligible expenditures would only be covered in special circumstances, if the project was approved. The use of pre-execution expenditures allowed NGOs to rapidly deploy in responding to RFAs.

Annex B – Audit Criteria

Governance

- An effective governance structure is in place to provide oversight and strategic direction for the programs.

- 1.1 The mandates, roles, responsibilities and accountabilities of the governance bodies are clearly defined, documented, communicated and understood.

- 1.2 Governance bodies are effectively designed to enable collaboration and support timely and informed decision making.

- 1.3 Monitoring and reporting processes are established and applied to ensure adequate oversight and timely decision making.

Controls

- Controls are designed and implemented to ensure compliance with relevant legislation; policy instruments; as well as agreement and program requirements.

- 2.1 Controls are in place to ensure that program and agreement documentation is in compliance with applicable legislation, policy instruments and frameworks.

- 2.2 Controls are in place to ensure contribution agreements are in compliance with the terms and conditions.

- 2.3 Performance indicators are identified, established, and reported on to inform program management.

- 2.4 Financial controls are in place to ensure that claims/payments are in compliance with the Financial Administration Act.

Annex C - Acts, Policies, Directives, Guidelines

Acts

- Financial Administration Act

- Public Safety Act

Treasury Board Approved Policies and Related Instruments

- Policy on Transfer Payments

- Directive on Transfer Payments

- Guideline on the Directive on Transfer Payments

Public Safety Directives and Related Instruments

- Delegation of Financial Signing Authorities (DFSA) Instruments

- DFSA Matrix

- DFSA Supporting Notes

- Funding Agreement Amendment Directive

- In-Kind Contribution Directive

- Pre-Execution Expenditures Directive

- Pre-Execution Expenditures Procedures

- Project Level Risk Management Directive

- Recipient Audit Policy

- Recipient Audit Directive

- Guidelines on Official Languages Requirements for Grant & Contribution Programs

- Guidelines on Performance Service Standards for Transfer Payment Programs

Annex D - Grant and Contribution Risk Mitigation Measures

Mitigation Strategies per the PS Project Level Risk Management Directive (2018)

| Activity | Low | Medium | High |

|---|---|---|---|

| Payments | Semi-Annual Progress Payments OR When advance payments are required:

|

Quarterly Progress Payments OR When advance payments are required:

|

Quarterly progress payments only. Quarterly advance payments are allowable when a program area deems this essential to meet the objectives of the funding agreement. NOTE: When it is necessary to meet the objectives of the funding agreement, an advance payment may be made at the beginning of any subsequent year to cover expenditures for April. However, no further advances should be made until the final cash flow of the prior fiscal year has been reconciled. |

| Financial Reporting Frequency |

|

|

|

| Non-Financial/Activity Reporting Frequency | Semi-Annual | Three Times a Year | Quarterly |

| Project Holdbacks | Minimum 3% of the overall PS funding | Minimum 5% of the overall PS funding | Minimum 10% of the overall PS funding |

Footnotes

- 1

As per the Terms and Conditions for the HWF program, large scale emergencies may include pandemics and natural disasters such as floods and wildfires.

- 2

As of June 2023, there were three COV19 and one HWF recipient audits that were either ongoing or planned as part of CMB’s the Departmental Three-Year Recipient Audit Plan. CMB is responsible for the Departmental Three-Year Recipient Audit Plan.

- 3

The requirement outlined in the Guidelines was removed as part of the February 2023 update.

- 4

Percentage of facilities which received assistance as a result of a request from public health authorities, which were effectively supported by the recipient.

- Date modified: